The disruption of the US import beer category

USA – After two decades as the top-selling beer in America, Bud light lost its title this year. Modelo Especial took over as the most popular beer tracked in retail channels. Everyone had a view why Bud Light was relegated to second place. But hardly anyone put it down to fundamental changes in consumer perceptions and the beer price architecture.

Ever since Bud Light was dethroned in early summer, pundits began offering their views. Some saw it as an indicator of AB-InBev’s inability to keep up with drinkers’ diversifying beer tastes. Some attributed it to demographic changes in the American population and the growing number of Hispanic consumers. Even more thought it was a well-deserved punishment for Bud Light, having partnered with transgender activist Dylan Mulvaney.

The truth is, Bud Light’s downfall has less to do with Bud Light and more with profound changes in the US beer market, especially within the import category, which has disrupted the beer categories.

Volumes down, revenues up

In 2010, the US brewing industry shipped 209.7 million barrels, but by 2020, that number had declined slightly to 209.2 million barrels, according to data by Beer Marketer’s Insights, a trade publication. Since then, total beer volume has fallen at a compound annual growth rate of 2 percent. However, due to consumers’ increasing preference for premium brands and products, dollar sales have continued to climb, even when volumes have not.

According to estimates by Beer Marketer’s Insights, the above premium segment, which includes imports, craft beers, and flavoured malt beverages (FMBs), accounted for more than 60 percent of beer category dollar sales in 2020.

Of course, in terms of volumes, the premium segment, which includes domestic brands like Bud Light, Miller Lite and Coors Light, plus the sub-premium/domestic value segment, still outsell the high-end segment handily. Per the website vinepair.com, domestic beer brands (premium and sub-premium) make up 64 percent of the market by volume, imports hold around 22 percent and “craft” the rest.

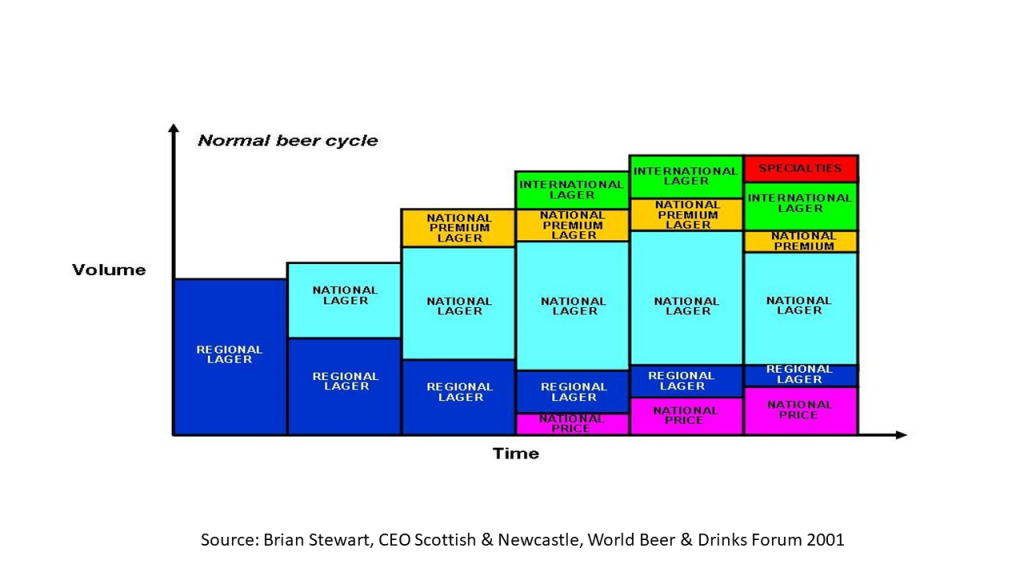

The long game of premiumisation

Some 20 years ago, there was consensus among pundits that beer markets, over time, would evolve in such a fashion that above premium brands (in those days imports, international brands, and “specialties” rather than “craft beer”) would eventually represent one in four bottles of beer being sold. This is what brewers mean when they talk about “premiumisation”.

Fast forward to today and the US market appears to have bested Mr Stewart’s projections. Bud Light is still a brand worth billions of dollars in revenue. Even after losing its crown to Modelo Especial, Bud Light remains the second best-selling beer by dollar sales and the best-selling by volume.

Just follow the lines

There is no denying, though, that it has seen its dollar sales swoon for years. Bump Williams, an intel firm, began to notice Bud Light and Especial’s convergent trends in 2020. Modelo Especial, a Pilsner served in a wide, gold-topped bottle, was expected to grow in the double digits, while Bud Light would decline in the single digits.

By extending those lines, Bump Williams predicted that Modelo Especial would surpass Bud Light in chain retail dollar sales in the next three to four years, that is in 2024/25. The Mulvaney fiasco simply speeded things up.

Nixing the life cycle theory

These trends were not lost on us observers from across the Atlantic. But we were customarily fobbed off with the explanation that Bud Light was just following its life cycle. No matter how skilful its marketers were, they could not arrest or reverse the trend. Once a brand reached maturity, a decline was kind of inevitable.

However, Bud Light’s dethroning is special and for two reasons. One, because it was a once second-tier Mexican import from Grupo Modelo that rose to become the new everyday beer of choice for grocery, liquor store, and convenience shoppers; and two, because Constellation’s sustained aggressive pricing had narrowed the price gap to Bud Light, thus persuading consumers to trade up to Modelo Especial.

You need to be a subscriber to Brauwelt International to continue reading this report.